May 1, 2026

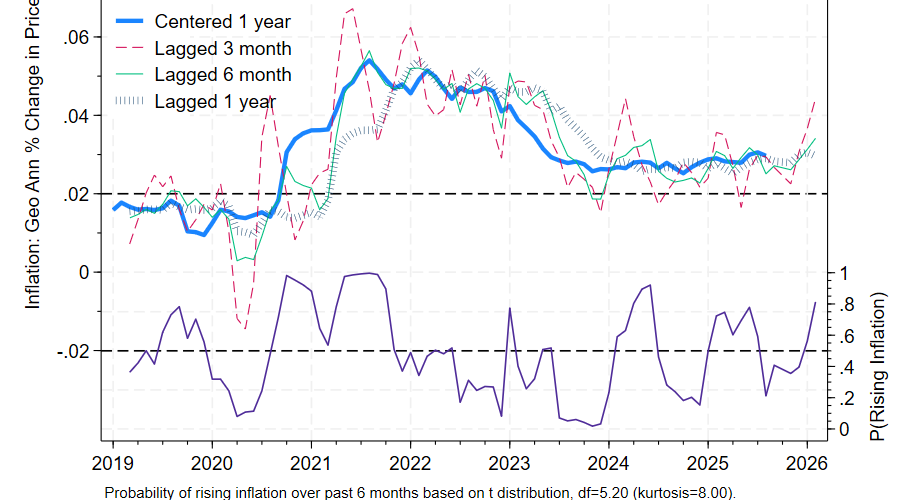

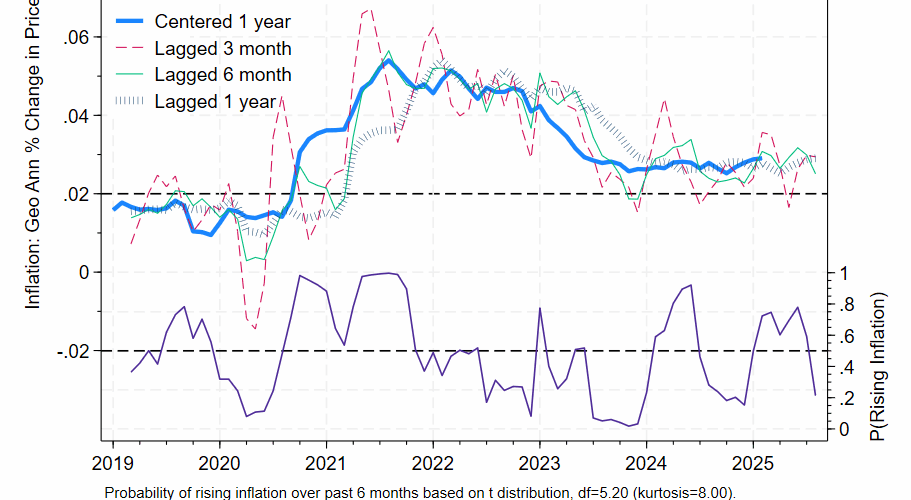

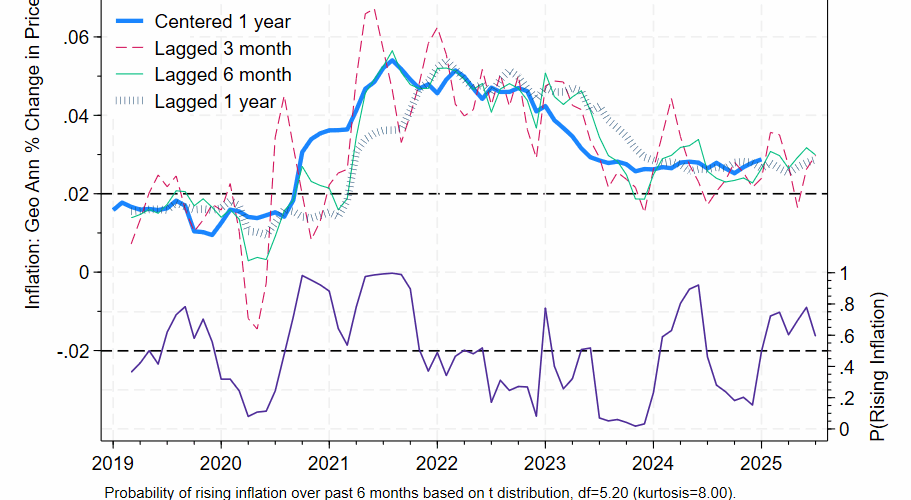

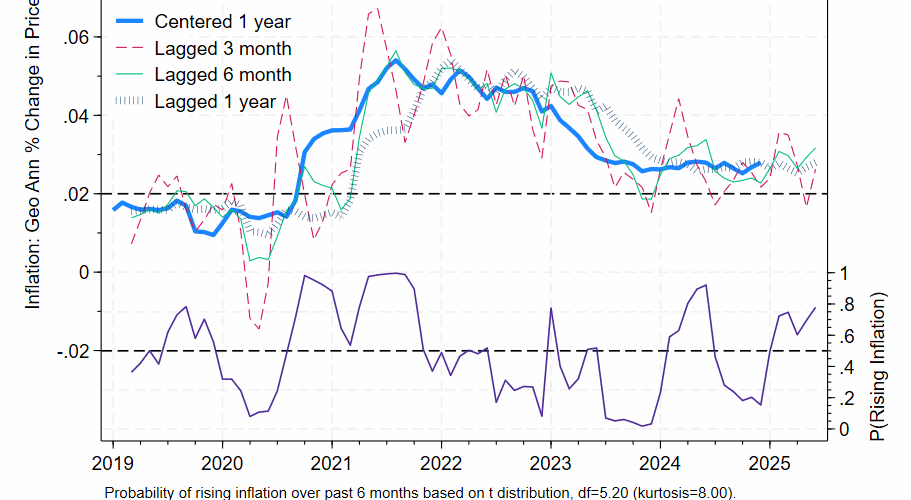

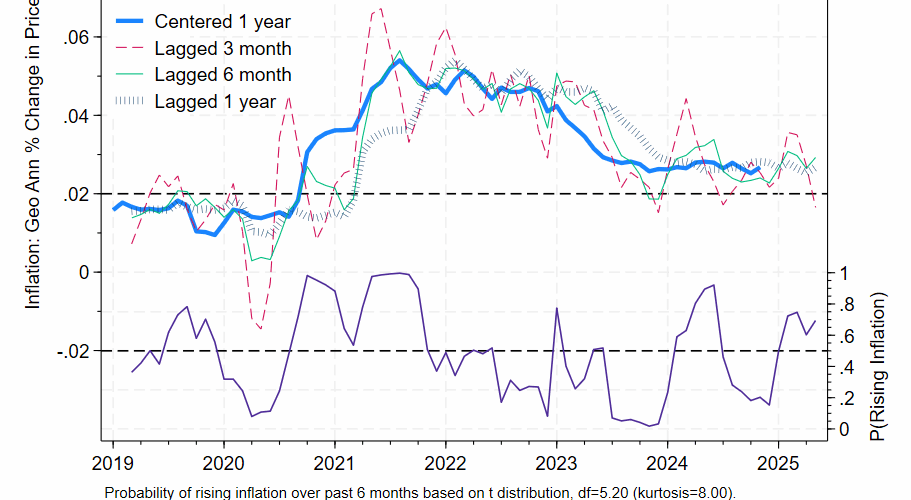

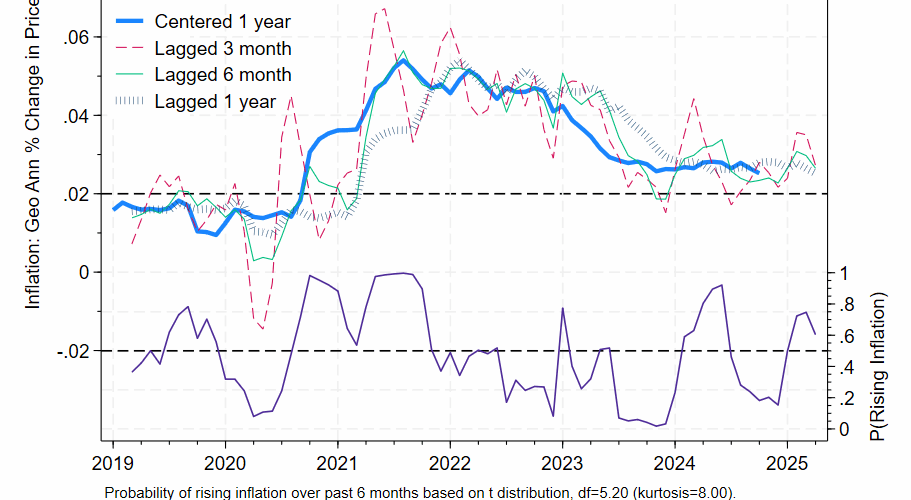

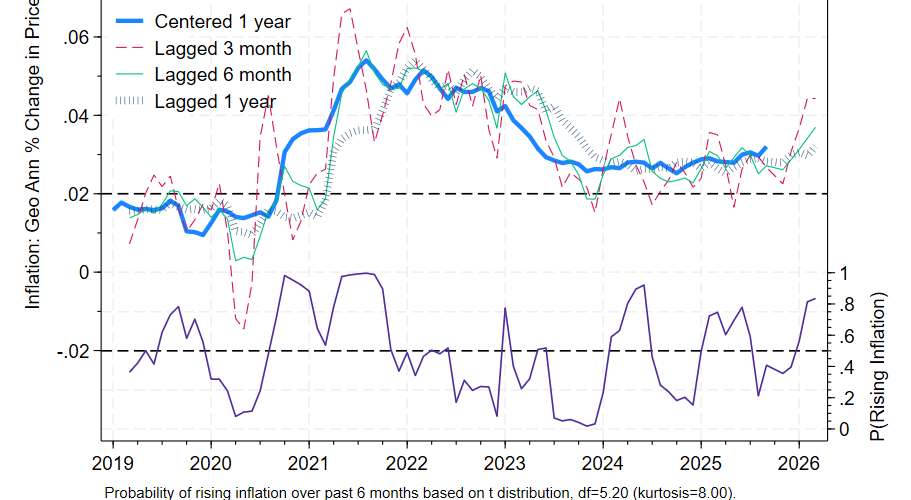

While 12 month Core PCE inflation was an above target 3.2% in March, the 6 month percentage change came in at 3.7%, which happens to be within the target Fed Funds range of 3.50 to 3.75%. Insofar as the 6 month lag is the best predictor of 1 year inflation centered on the current month, the real fed funds rate is currently close to zero.

Core PCE inflation also appears to be rising: current one year inflation tells us what inflation centered in Sep 2025 was: it was 3.2% or a half a percentage point lower than 3.7%.

Press reports assert a divided Fed, with dissenting board members wanting to drop language implying an easing bias. Outgoing Chairman Powell stated in his press conference, “Nobody’s calling for a hike right now.”

I predict the next change in the Federal Funds target will be in an upward direction (>80% subjective probability) and opine that the Fed should prepare for such an eventuality in its public communications. It would be prudent for the Fed to consider a quarter point rise during the next meeting, subject to upcoming developments, consultation with petroleum experts regarding the longevity of this shock, and its dual mandate. The FOMC properly considers a range of factors, but this indicator at least is flashing yellow.

ETA May 2: I have to retract my forecasted Fed hike. Odds of recession are elevated as long as world oil output is limited by the Iran War. Inventory draw-downs have been covering much of the gap between oil demand and supply, but that can’t last indefinitely. Supply shocks pose special challenges for monetary authorities.